Var Formula : Portfolio Variance Formula Example How To Calculate Portfolio Variance / Formula var abbreviation meaning defined here.. The second demonstrates that the var formula is also capable of using references to cells that store numbers. Keep these three parts in mind as we give some examples of variations of the question that var answers: It estimates how much a set of investments might lose (with a given probability), given normal market conditions, in a set time period such as a day. This composite cell range consists of all the values from a2 through a11. 0 ratings0% found this document useful (0 votes).

But it is actually very difficult to find on the web, and tedious to derive. Properties, constants, operators and functions. Hello, i'm confused about a very easy question, how to calculate the lognormal var. So, without knowing what is your goal with this calculation i figured out some syntax mistakes. Where x is the sample mean average(number1,number2,…) and n is the sample size.

Var P Function In Excel Datascience Made Simple from www.datasciencemadesimple.com A time period, a confidence level and a loss amount (or loss percentage). So, without knowing what is your goal with this calculation i figured out some syntax mistakes. Savesave var formula for later. It seems i need to get a distribution of n(0.551) = 0.128. Calculation of var requires one to make some assumptions and use them as inputs. Example 23.4) on how to the credit var formula is used. What does var stand for in formula? Example 23.4) which shows how the credit var formula is applied.

Here you are the question and answer:

Locationcounts = var final_total =. What is the most i can—with a 95% or 99% level of confidence—expect to lose in. The measure is often applied to an investment portfolio for which the calculation gives a confidence interval about the likelihood of exceeding a certain loss threshold. This composite cell range consists of all the values from a2 through a11. A measure of spread for a distribution of a random variable that determines the degree to which the values of a random variable differ from the expected value. Calculation of var requires one to make some assumptions and use them as inputs. I can't seem to get the same answer as the example (i.e. Var.s assumes that its arguments are a sample of the population. Let us take the example of a classroom with 5 students. I am trying to write the following var formula but keep on getting an error, cannot see the wood for the trees. Here we discuss steps for calculation of p value, z statistic with practical examples and downloadable excel template. Hello, i'm confused about a very easy question, how to calculate the lognormal var. Var of a single asset is the value of the asset multiplied by its volatility.

Where x is the sample mean average(number1,number2,…) and n is the sample size. Example 23.4) on how to the credit var formula is used. But it is actually very difficult to find on the web, and tedious to derive. Keep these three parts in mind as we give some examples of variations of the question that var answers: By the basic definition of the var, it is the maximum expected potential loss on the portfolio over the given time horizon for a given confidence interval under normal market conditions(jorion,2001).

Frm Bond Returns Value At Risk Var As Bond Risk Youtube from i.ytimg.com In the normal distribution, 95% confidence level is. Value at risk (var) is a measure of the risk of loss for investments. But it is actually very difficult to find on the web, and tedious to derive. I am trying to write the following var formula but keep on getting an error, cannot see the wood for the trees. In chapter 23 of hull's options, futures, and derivatives he has an example (i.e. Var uses the following formula: Var is not only applicable in exploring the market risk but also in manage all other types of risk. 0.128) since i keep on getting n(±3.1951) or n(±1.1351).

The variance of two random variables, x+y is in the beginning of every statistics book.

In chapter 23 of hull's options, futures, and derivatives he has an example (i.e. That data is used by investors to make decisions and set a strategy. In the third example, instead of sending multiple values or references, we have passed a single composite range. The var measurement shows a normal distribution of past losses. Var uses the following formula: A useful formula, where a and b are constants, is the standard deviation of x is the square root of var(x). Simple calculations like arithmetic (add/subtract) and logic (true/false). Var.s assumes that its arguments are a sample of the population. Var of a single asset is the value of the asset multiplied by its volatility. A time period, a confidence level and a loss amount (or loss percentage). Value at risk (var) is a measure of the risk of loss for investments. Keep these three parts in mind as we give some examples of variations of the question that var answers: Var measures the potential loss that could happen in an investment portfolio over a period of time.

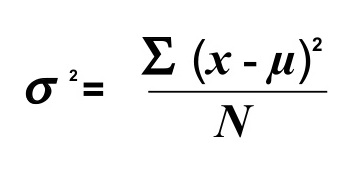

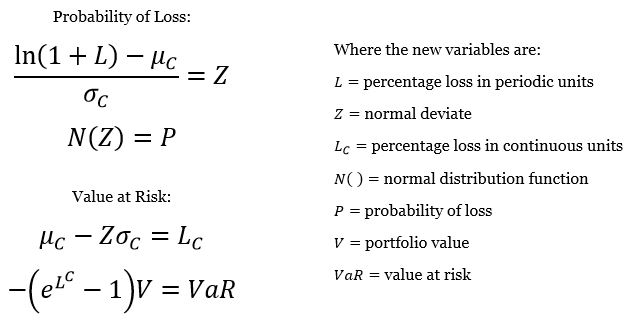

Here we discuss steps for calculation of p value, z statistic with practical examples and downloadable excel template. It seems i need to get a distribution of n(0.551) = 0.128. Calculation of var requires one to make some assumptions and use them as inputs. The variance of random variable x is often written as var(x) or σ2 or σ2x. The annual mean and volatility of a portfolio are 12% and 30 as i understood, the formula should be.

Value At Risk India Dictionary from 1investing.in So, without knowing what is your goal with this calculation i figured out some syntax mistakes. When you create a new formula, there are four options to choose from: If the assumptions are not valid, then neither is the var figure. But it is actually very difficult to find on the web, and tedious to derive. In chapter 23 of hull's options, futures, and derivatives he has an example (i.e. Keep these three parts in mind as we give some examples of variations of the question that var answers: Var.s assumes that its arguments are a sample of the population. A useful formula, where a and b are constants, is the standard deviation of x is the square root of var(x).

Example 23.4) which shows how the credit var formula is applied.

In chapter 23 of hull's options, futures, and derivatives he has an example (i.e. Variance formula examples show how to use var, var.s, var.p, vara and other functions. These are effectively your variables. operators: 0.128) since i keep on getting n(±3.1951) or n(±1.1351). Here you are the question and answer: Var of a single asset is the value of the asset multiplied by its volatility. For formulas to show results, select them, press f2, and then press enter. In the third example, instead of sending multiple values or references, we have passed a single composite range. In the normal distribution, 95% confidence level is. Var.s uses the following formula: The measure is often applied to an investment portfolio for which the calculation gives a confidence interval about the likelihood of exceeding a certain loss threshold. Here we discuss steps for calculation of p value, z statistic with practical examples and downloadable excel template. Includes links to web pages that the correct formula for degrees of freedom (df) depends on the situation (the nature of the test statistic, the number of samples, underlying.

0 Komentar